Table of Contents

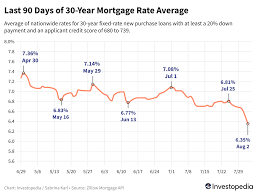

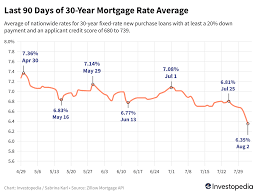

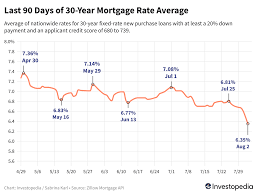

As of August 13, 2024, mortgage rates for both 15- and 30-year fixed-rate loans are holding steady at their lowest levels in over a year. This trend is providing a significant opportunity for homebuyers and those looking to refinance, as lower can lead to substantial savings over the life of a loan. The stability in rates comes amid economic conditions that include a cooling housing market and efforts by the Federal Reserve to manage inflation.

Impact of Low Mortgage Rates

The continuation of low mortgage rates has several implications for the housing market and broader economy:mortgage rates

- Increased Affordability: Lower mortgage rates reduce the monthly payment burden on borrowers, making homeownership more accessible for many people. This can stimulate demand in the housing market, especially among first-time buyers who are more sensitive to changes in affordability.

- Refinancing Opportunities: Homeowners with existing mortgages may take advantage of the low rates by refinancing their loans. Refinancing can lower monthly payments, reduce the total interest paid over the life of the loan, or even allow homeowners to cash out equity for other expenses.

- Impact on Housing Prices: While low rates make borrowing cheaper, they can also contribute to higher home prices as more buyers enter the market. This dynamic creates a competitive environment, which may drive up prices, particularly in markets with limited housing inventory.

- Economic Growth: Low can stimulate the economy by encouraging consumer spending. When homeowners refinance at lower rates, they often have more disposable income to spend on goods and services, which can boost economic activity.

- Investor Activity: Investors may also be drawn to the real estate market due to the attractive borrowing costs, potentially increasing the demand for investment properties. However, this can also lead to concerns about real estate bubbles in certain regions.

Factors Influencing Current Mortgage Rates

Several factors contribute to the current low mortgage rates:

- Federal Reserve Policy: The Federal Reserve’s monetary policy plays a crucial role in influencing mortgage rates. Efforts to control inflation while supporting economic growth have led to a cautious approach to interest rate hikes, keeping mortgage rates relatively low.

- Economic Indicators: Key economic indicators such as inflation, employment data, and GDP growth influence investor sentiment and bond yields, which in turn affect. Recent data suggesting a stabilizing economy with controlled inflation has contributed to the persistence of low rates.

- Global Economic Conditions: Global economic events, such as geopolitical tensions or fluctuations in foreign markets, can also impact U.S. mortgage rates. Investors often seek safer investments like U.S. Treasury bonds during uncertain times, driving down yields and, consequently, mortgage rates.

Considerations for Homebuyers and Homeowners

For those in the market for a new home or considering refinancing, the current low present a significant opportunity. However, there are important factors to consider:

- Loan Terms: Homebuyers should carefully evaluate the terms of their mortgage, including the interest rate, loan type (fixed vs. adjustable), and the duration of the loan. A fixed-rate mortgage offers stability in payments, while an adjustable-rate (ARM) might start with a lower rate but carries the risk of rate increases in the future.

- Closing Costs: When refinancing, it’s essential to consider the closing costs assocated with the new loan. While refinancing at a lower rate can save money over time, the upfront costs must be weighed against the potential savings.

- Market Timing: While current rates are low, they can fluctuate based on economic conditions and Federal Reserve policy decisions. Potential homebuyers should stay informed about market trends and consider locking in a rate if they believe rates might rise.

- Affordability and Budgeting: Even with low it’s important for buyers to assess their overall financial situation, including how much they can afford to borrow without overextending themselves. A thorough review of income, debt, and future financial goals is crucial before committing to a mortgage.

Future Outlook for Mortgage Rates

Looking ahead, the trajectory of mortgage rates will depend on several factors, including:

- Federal Reserve Actions: The Federal Reserve’s decisions on interest rates will continue to be a major determinant of mortgage rate trends. If inflation pressures increase, the Fed might raise rates more aggressively, which could push mortgage rates higher.

- Economic Performance: Continued economic growth, stable employment, and controlled inflation could keep mortgage rates low in the near term. However, any significant economic downturn or unexpected inflation spikes could lead to rate volatility.

- Housing Market Dynamics: The housing market’s response to current rates, including changes in demand, housing inventory, and price trends, will also influence future rate movements. A balanced market could maintain rate stability, while significant shifts in demand could cause fluctuations.

Conclusion

The sustained low mortgage rates as of August 13, 2024, offer significant opportunities for homebuyers and homeowners alike. While these rates present an attractive chance to secure lower borrowing costs, it’s important for individuals to carefully consider their financial situation, loan options, and market conditions before making decisions. As the economic landscape continues to evolve, staying informed and prepared will be key to maximizing the benefits of these favorable rates.